Remuneration of Director as per companies Act 2013

Introduction

In a company, there can be many types of directors such as Managing Director, Whole-time Director, Part-time Directors and managers. The remuneration shall be paid all of the directors in accordance with provisions of section 197 of the companies act, 2013. In the old companies act, 1956 there were provisions under chapter 198,309 etc which dealt with Managerial remunerations separately whereas the new companies act, 2013 consolidated all these provisions under one chapter i.e 197. With the appointment of Directors, there is some remuneration set by the act which should not be forgotten. This article will let you know the Remuneration of Director as per companies Act 2013.

Applicability of Remuneration of Director

Being a Director of a company, it is important to be aware of the managerial remuneration prescribed as per Companies Act, 2013. Whether it is a private limited company or a Public limited company, in both the cases regulations for payment of directors will be followed.

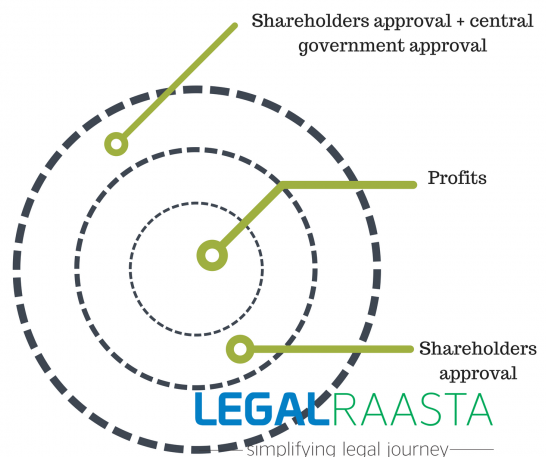

Three ways of Managerial Remuneration are described by the following figure:

- Automatically by Profits

- By Shareholders’ Approval

- By Shareholders’ and Central Government

Remuneration of Director under section 197 of the companies act 2013

The various methods at which company can pay remuneration to its director is below:

- In case of Public company, a company can pay not more than 11% of the net profit as calculated in a manner laid down in section 198 of the companies act. Whether it is Managing director or whole time directors.

- A company having only one managing director, whole-time director or manager shall not pay more than 5% of its net profits.

- A company has more than one such directors, remuneration shall be payable not more than 11% of the net profit.

Maximum remuneration for a Director:

The table given below will further portray the limits:

| Capital (Rupees) | Highest limit for Remuneration to a Director |

|---|---|

| Less than 5 crores | 30 lakhs |

| 5 crore or more but less than 100 crore | 42 lakhs |

| 100 crore or more but less than 250 crore | 60 lakhs |

| 250 crore and above | 60 lakhs along with 9.99% of the capital in excess of Rs. 250 crore |

- If a company is having an adequate profit then it can pay to its managing director or whole time manager remuneration up to 200% of the above mentioned managerial remuneration if shareholders have given their approval through a special resolution.

- A managerial director who is not holding share up to Rs. 5 lakhs or more and director of the company is not related to any promoter during the period of two years prior to his appointment as a managerial person, so in this case, the company may pay to him 2.5% of the current relevant profits and up to 5% with the approval of shareholders by a special resolution.

- Current relevant profit is the profit calculated under section 198 and under this there is no deduction of an excess of expenditure over income as prescribed in section 4(1). It is relating to all usual working charges in respect of those years during which the managerial person was not an employee, director or shareholder of the company or its holding and subsidiary companies.

- While computing of the ceiling on remuneration specified in section II and section III, following are the perquisites which shall not be included:

- PF or superannuation fund or annuity fund are not taxable under the Income-tax Act, 1961 (43 of 1961).

- Gratuity shall not be exceeding half a month’s salary for each year of service

- Encashment of leave at the end of the tenure.

5. According to clause (a), any contribution made to PF (Provident fund), superannuation fund or annuity fund more than the limits of tax under IT Act 1961, shall not be included for the purpose of calculation of managerial remuneration. Whether it is an event of adequate profit or nil profit.

Facilities provided by the company as a Remuneration of director

It is not necessary that everything which is in the form of salary will be considered as remuneration. But apart from this, rewards and compensation provided to a managerial person are also countable in the remuneration. Following are the expenditure incurred by the company are also termed as managerial remuneration:

- Expenditure on rent-free accommodation, or any other amenity free of charge

- Expenditure on amenities at a concessional rate

- Expenditure on the life insurance, any pension, annuity or gratuity for the director or for his/her spouse/child.

- Expenditure on Indemnify on behalf of Director against any liability in respect of any negligence, default, misfeasance, breach of duty/trust then, in this case, the premium paid on such insurance would be taken as a part of its remuneration.

- Expenditure on maintenance of vehicles pertaining to personal use by director or manager.

For further more information regarding Company registration, Types of Business Forms, regulations governing companies you can visit our website: Legal Raasta

You can send your query on Email: contact@legalraasta.com and ring us on +918750048585.

Related Articles:

Related Posts

Our Clients

Featured In